Get Click Media

AI Communication Platform

Trusted by 10,000+ businesses

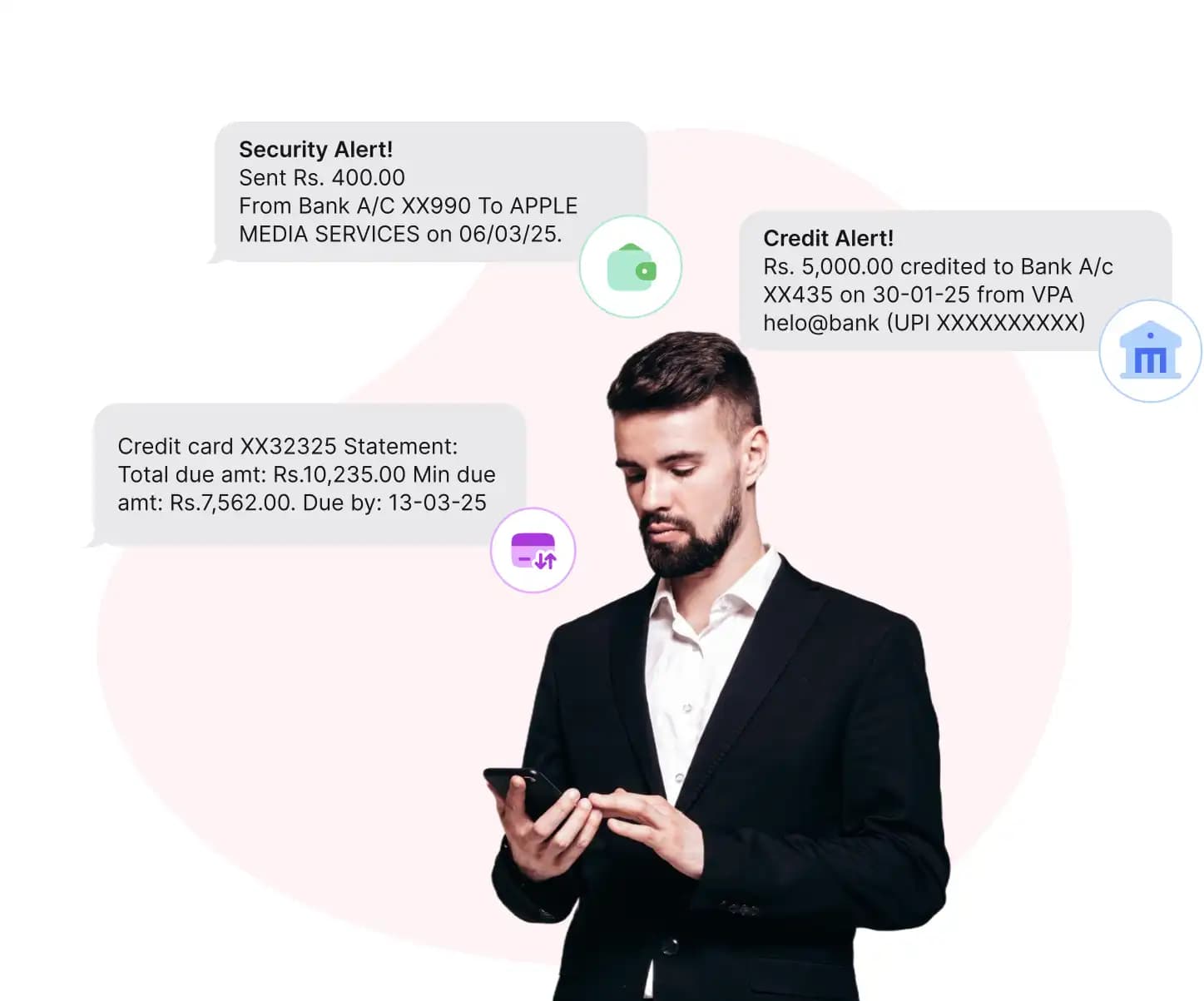

Banking and financial services communication in India has a trust problem. RCS Business Messaging solves it with Google-verified brand identity — your bank's name, logo, and verification checkmark on every message. Anti-phishing built into the channel itself.

Key result: Banks using RCS report 43% fewer phishing support calls and 4x–6x higher loan application rates vs SMS.

4x–6x

Higher loan application rate vs SMS

89%

Read rate for banking RCS messages

43%

Reduction in phishing-related support calls

0

DND restrictions on RCS vs SMS

India's banking sector loses an estimated ₹1,000 crore annually to SMS-based financial fraud. Banks have had their Sender IDs spoofed by fraudsters. RCS addresses this with verified sender identity — your bank's logo, name, and Google-verified checkmark on every message.

RCS is not classified as commercial SMS under TRAI regulations. Banks can send pre-approved loan offers at 7 AM to DND-registered customers — with full brand verification. No 9 AM–9 PM window restriction.

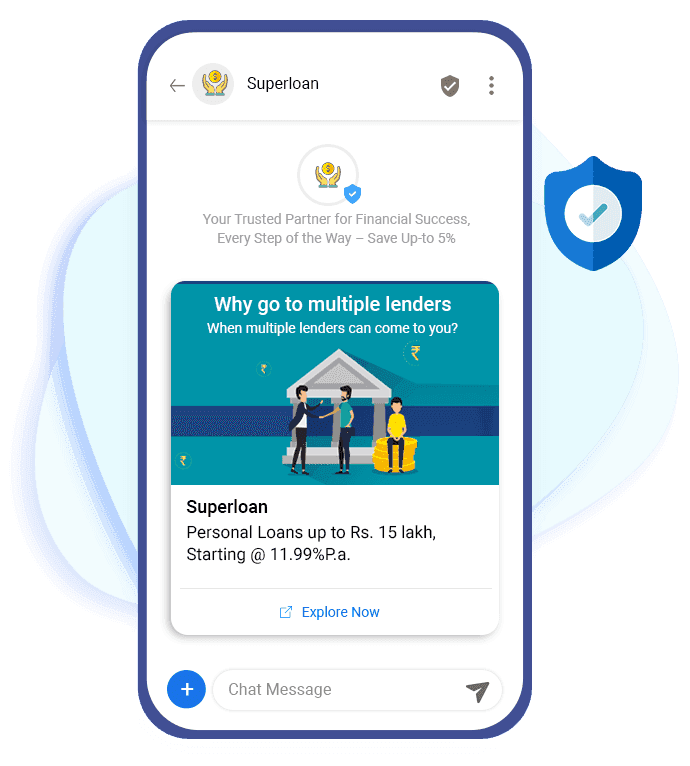

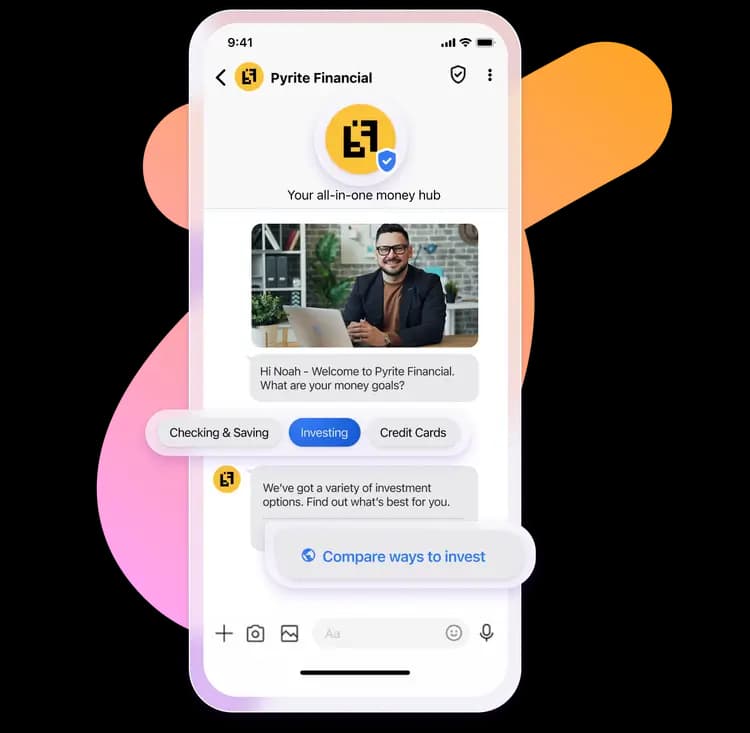

A 160-character SMS cannot present the features of a financial product. RCS rich cards show the card image, welcome bonus, key benefits, and an Apply Now button — product discovery in the messaging inbox.

The opportunity: Indian banking customers are conditioned to distrust unverified SMS. RCS restores trust through verified sender identity — and delivers 4x–6x higher conversion rates than SMS for credit cards and loans.

Here are the 10 most effective ways Indian banks, NBFCs, and financial institutions are using RCS messaging.

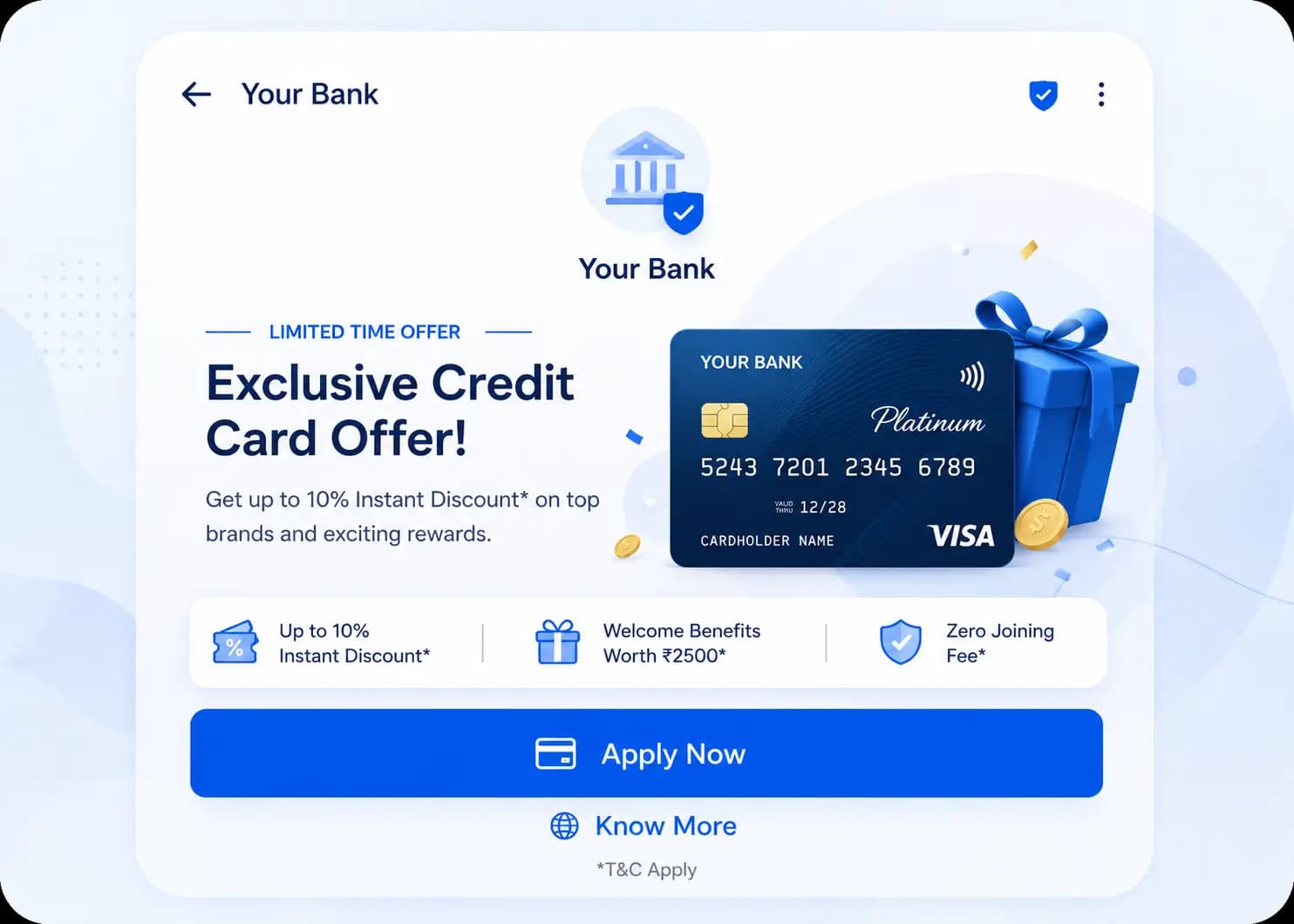

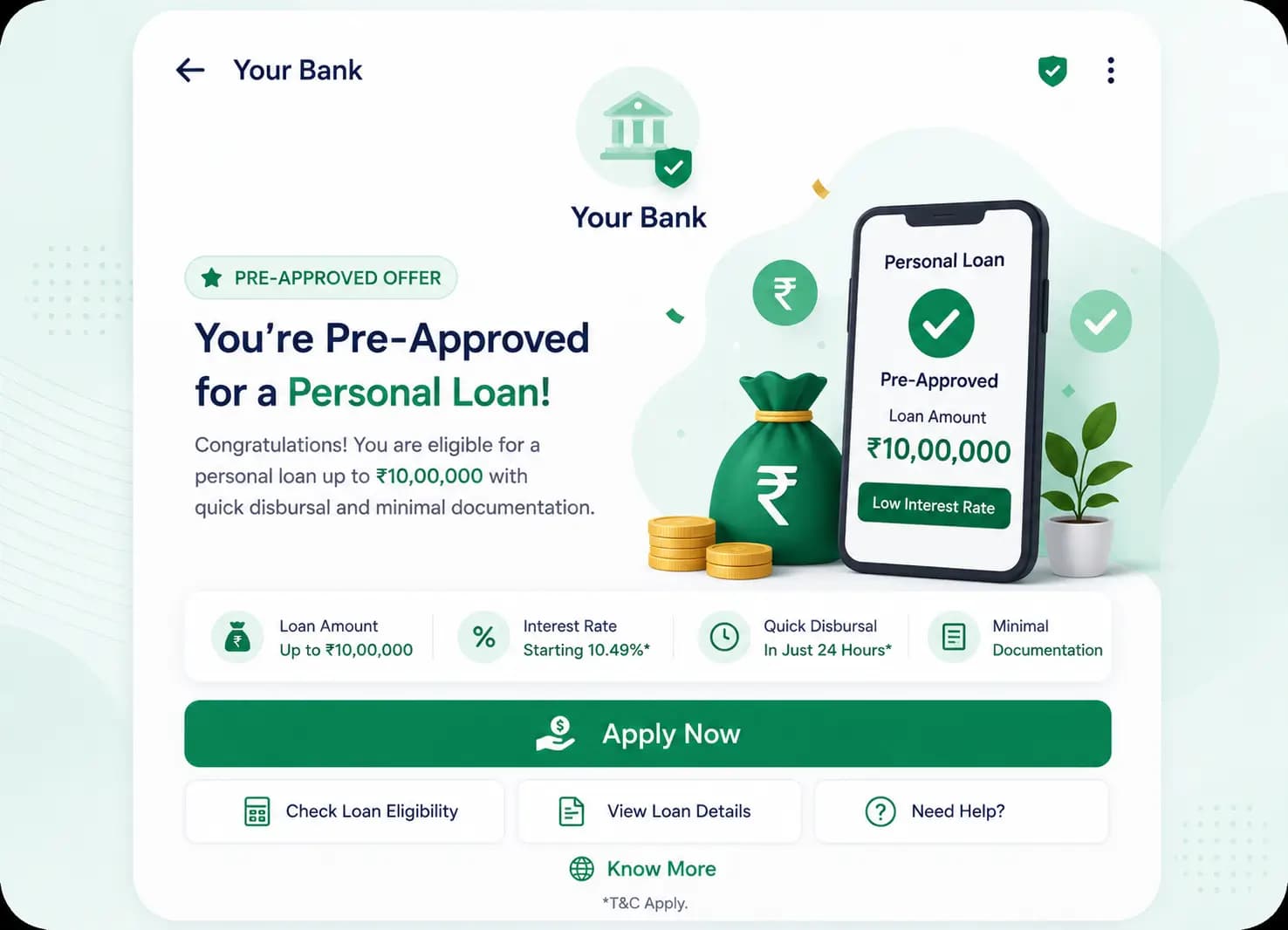

Trigger: Targeted offer to pre-qualified customers based on credit score, income, and transaction history. Sent Monday-Wednesday, 7–9 PM.

RCS format: Rich card with card image, card name, key benefits, joining fee, welcome bonus, and 2 buttons: 'Apply Now', 'See All Benefits'.

Result: Application rate: 6.2% vs SMS 1.1%. Cost per application: ₹38 vs ₹210 via SMS. Apply Now CTR: 31%.

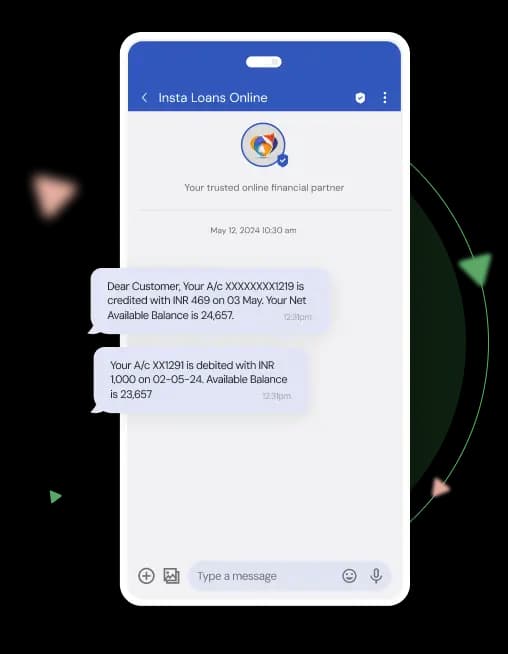

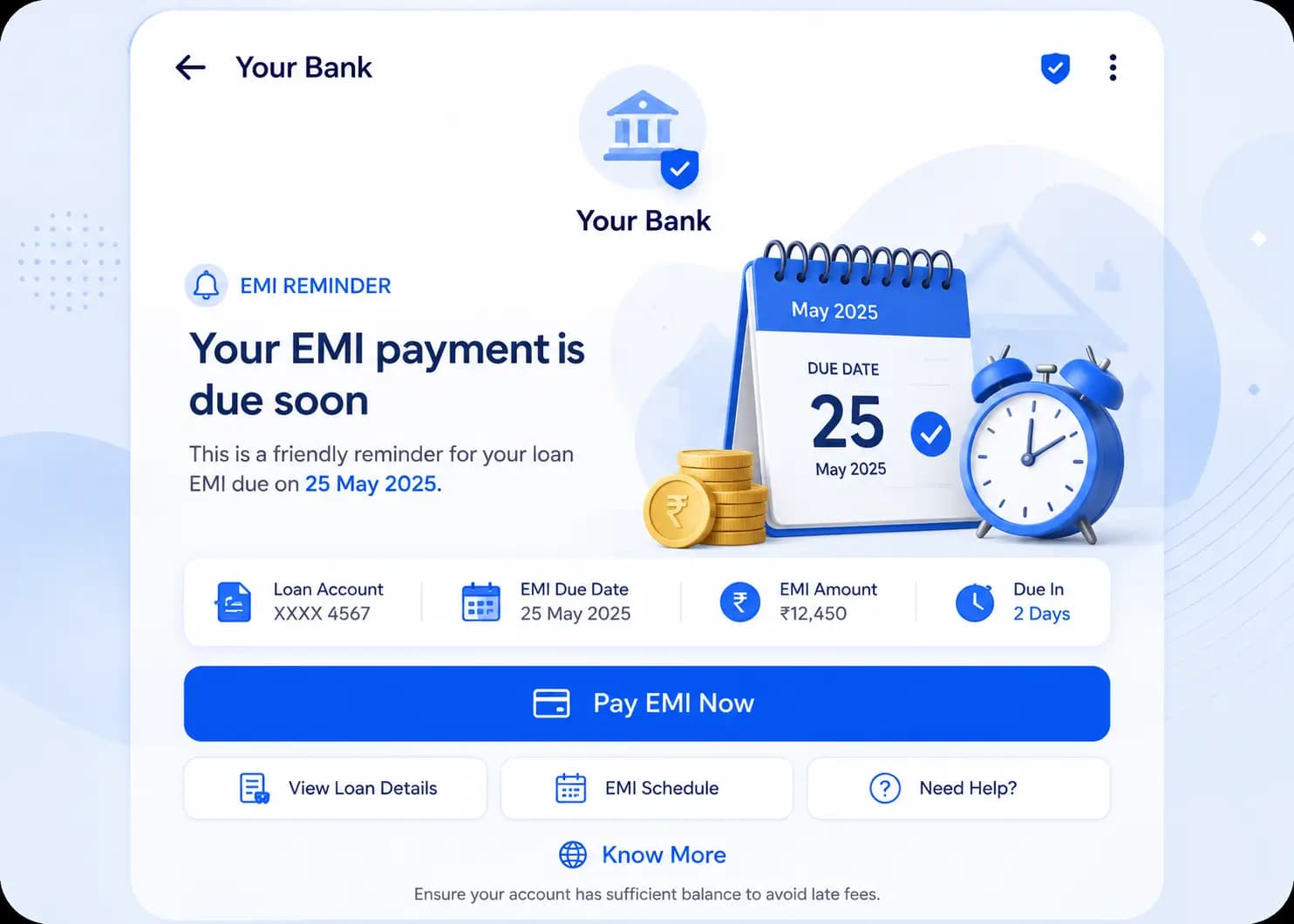

Trigger: 3 days before EMI due date for personal loans, home loans, auto loans, credit card outstanding. Transactional communication — no DND restriction.

RCS format: Rich card: bank logo + verified, loan/card type, EMI amount, due date, masked account number, 2 buttons: 'Pay Now' (links to payment portal), 'Set Up Auto-Pay'.

Result: On-time payment rate: +24% vs SMS reminder. 'Pay Now' button resolves 71% of cases without agent call. Delinquency reduction: 18% in 90-day cohorts.

Trigger: Pre-qualified customers identified by credit model. Highest conversion window: within 48 hours of salary credit or large incoming transfer.

RCS format: Rich card: bank logo + verified, pre-approved loan amount, interest rate, tenure options, EMI preview, 2 buttons: 'Apply in 2 Minutes', 'Calculate EMI'.

Result: Conversion rate: 8.4% vs SMS 1.9%. Disbursal rate within 24 hours: 62%. Cost per disbursed loan (RCS): 67% lower than branch-led acquisition.

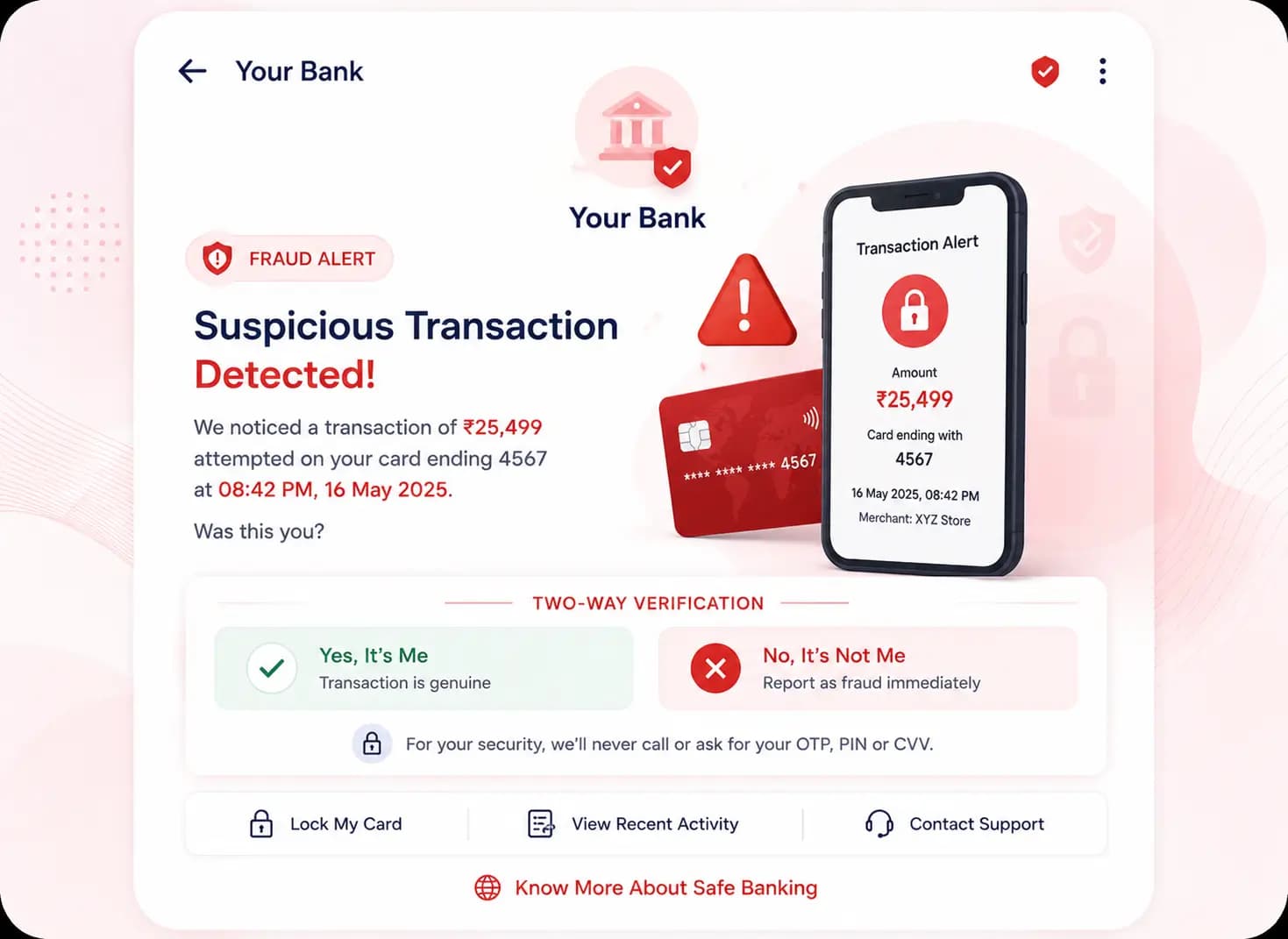

Trigger: Real-time trigger: unusual transaction detected. Immediate automated send — sub-30 seconds from trigger.

RCS format: Rich card: bank logo + verified, transaction details (merchant, amount, time, location), 3 quick-reply chips: 'Yes, this was me', 'No, block this transaction', 'Call Fraud Team'.

Result: Customer response rate: 67% vs SMS fraud alerts 12%. False positive friction reduced 44%. Fraud loss reduction: 29% for participating banks.

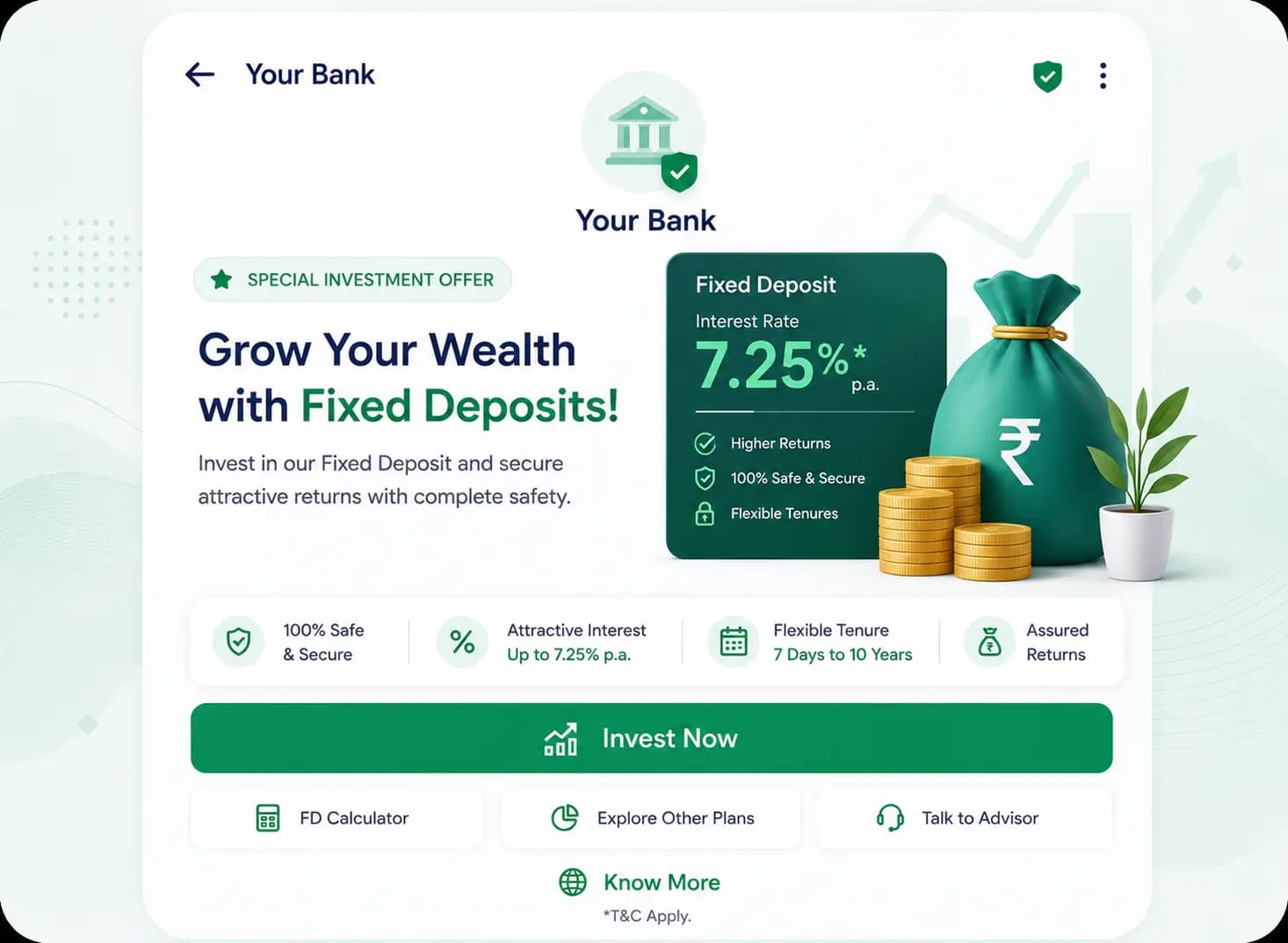

Trigger: Triggered by large balance sitting idle in savings account, FD maturity approaching, or quarterly investment campaign.

RCS format: Rich card: bank/product logo, investment type (FD, RD, SGB, mutual fund), interest rate, minimum amount, tenure options, 2 buttons: 'Invest Now', 'Talk to RM'.

Result: FD booking rate via RCS: 4.1% vs email 0.8%. 'Talk to RM' chip generates 2.8x more RM-initiated conversations than cold calls.

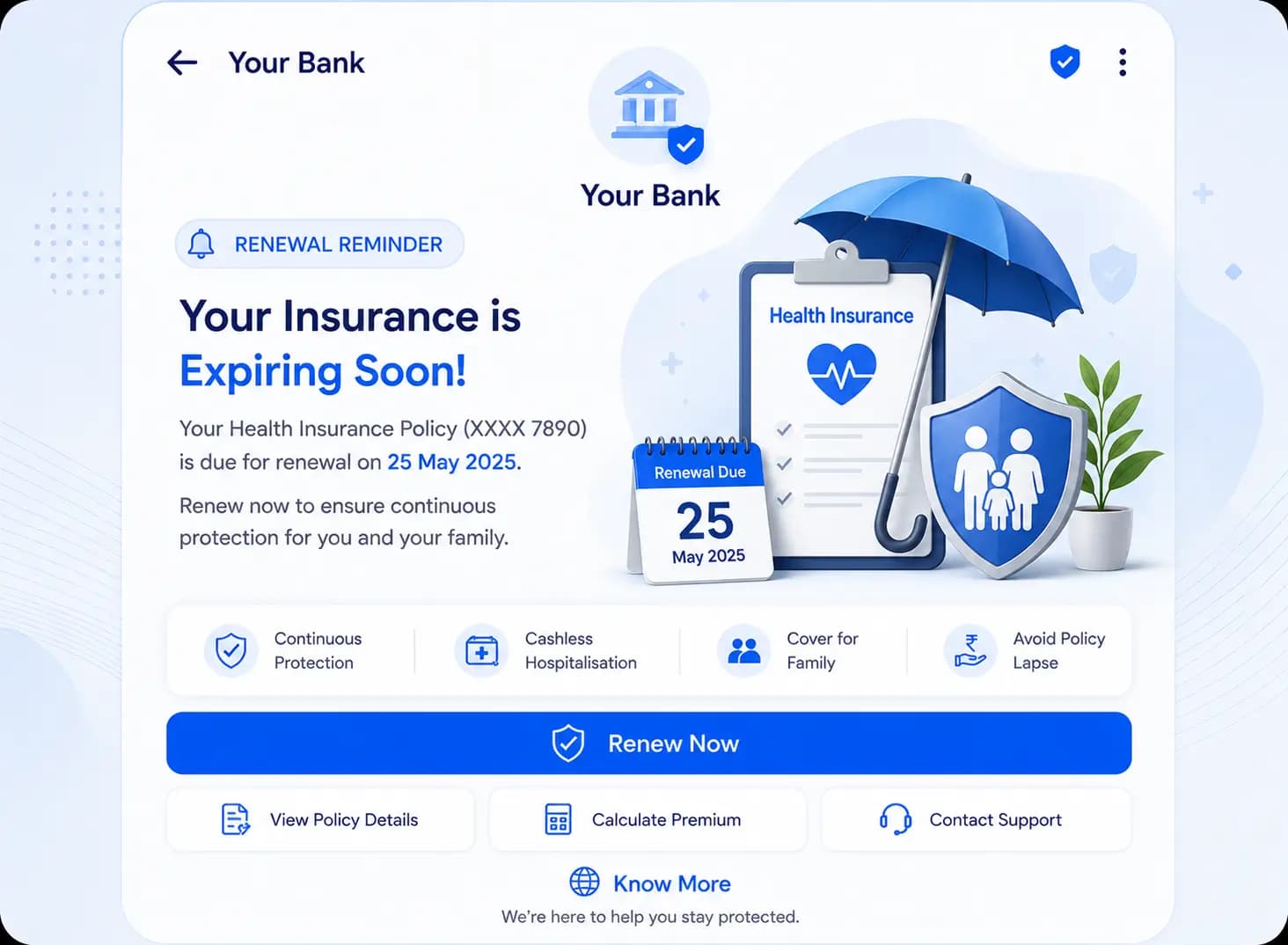

Trigger: 30 days, 15 days, 7 days, and 1 day before policy expiry. Sent by insurer or bancassurance partner.

RCS format: Carousel: Card 1 — policy summary (coverage, premium, expiry), Card 2 — what you lose if lapsed, Card 3 — renew now + new plan upgrade options. Buttons: 'Renew Now', 'View Policy', 'Compare Plans'.

Result: Renewal rate: +31% vs SMS reminder. 'Compare Plans' button drives 18% upgrade rate. Policy lapse rate: -29% for customers receiving RCS renewal series.

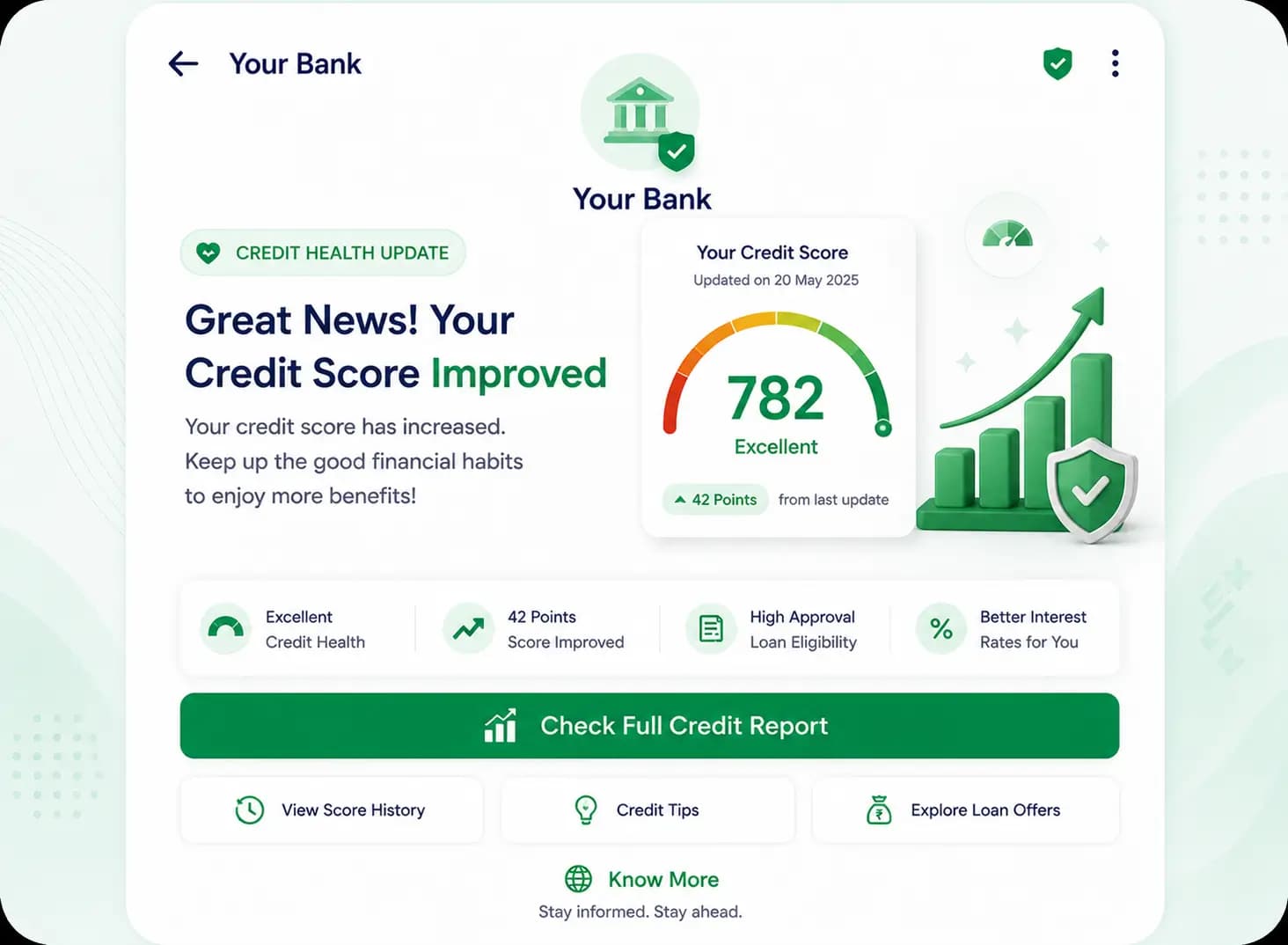

Trigger: Monthly credit score update notification. Triggered by score change >10 points. High-engagement touchpoint.

RCS format: Rich card: credit score gauge image, score change indicator (+/-), score category, 2 buttons: 'View Full Credit Report', 'Tips to Improve Score'.

Result: Open rate: 91% (highest of any banking RCS message type). CTR to credit report: 48%. Credit-score-linked loan offer conversion: 3.2x higher than non-personalised campaigns.

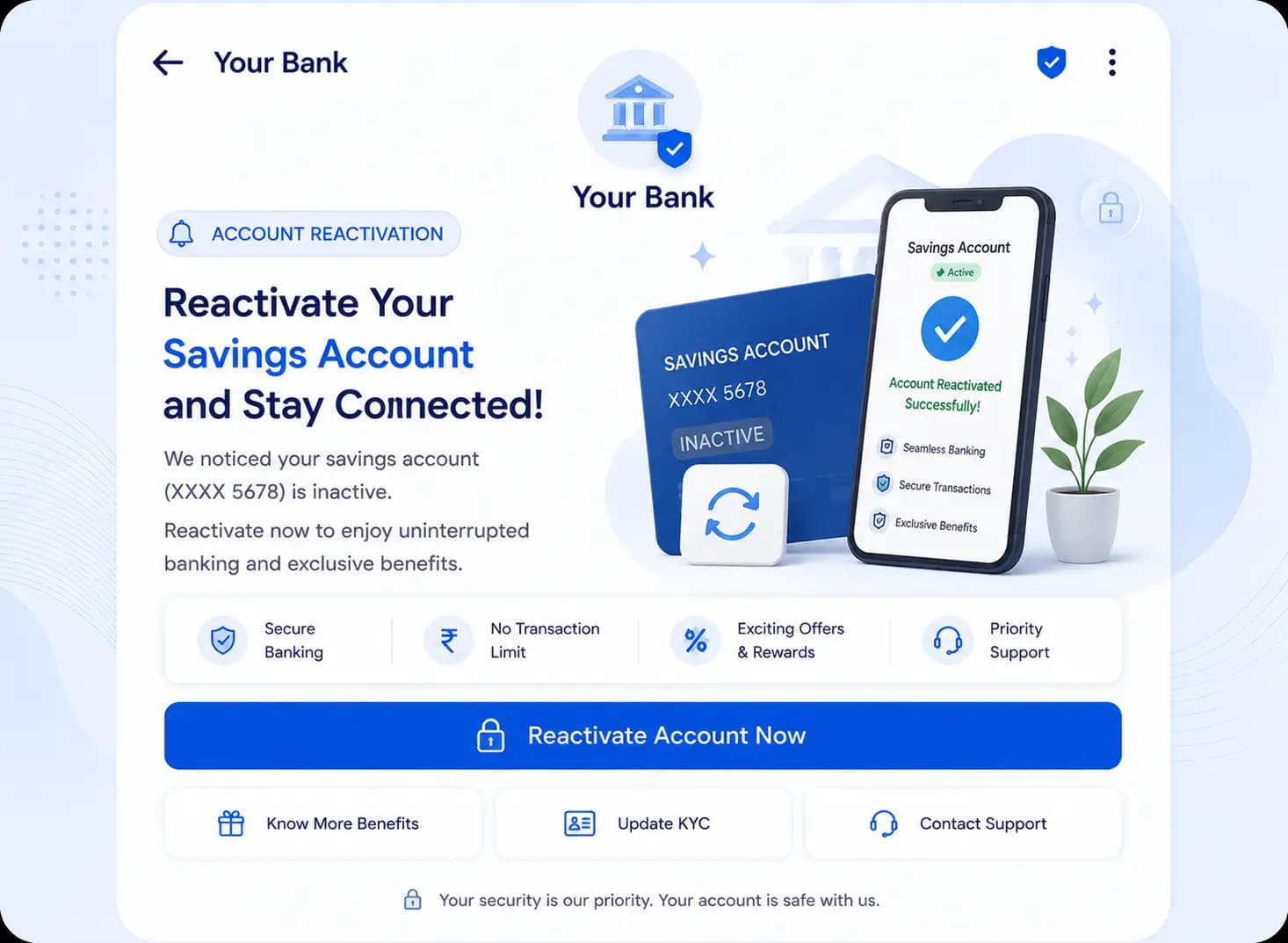

Trigger: Account dormant for 6+ months or zero transaction in last 90 days. Reactivation campaign with incentive.

RCS format: Rich card: bank logo + verified, account balance, dormancy status, reactivation incentive, 2 buttons: 'Reactivate My Account', 'Contact Branch'. Include Google Maps branch locator button.

Result: Reactivation rate via RCS: 14% vs email 2.3%. 'Find Branch' map button: 38% of reactivation visits use the map button. Cost per reactivated account: 76% lower than branch outreach.

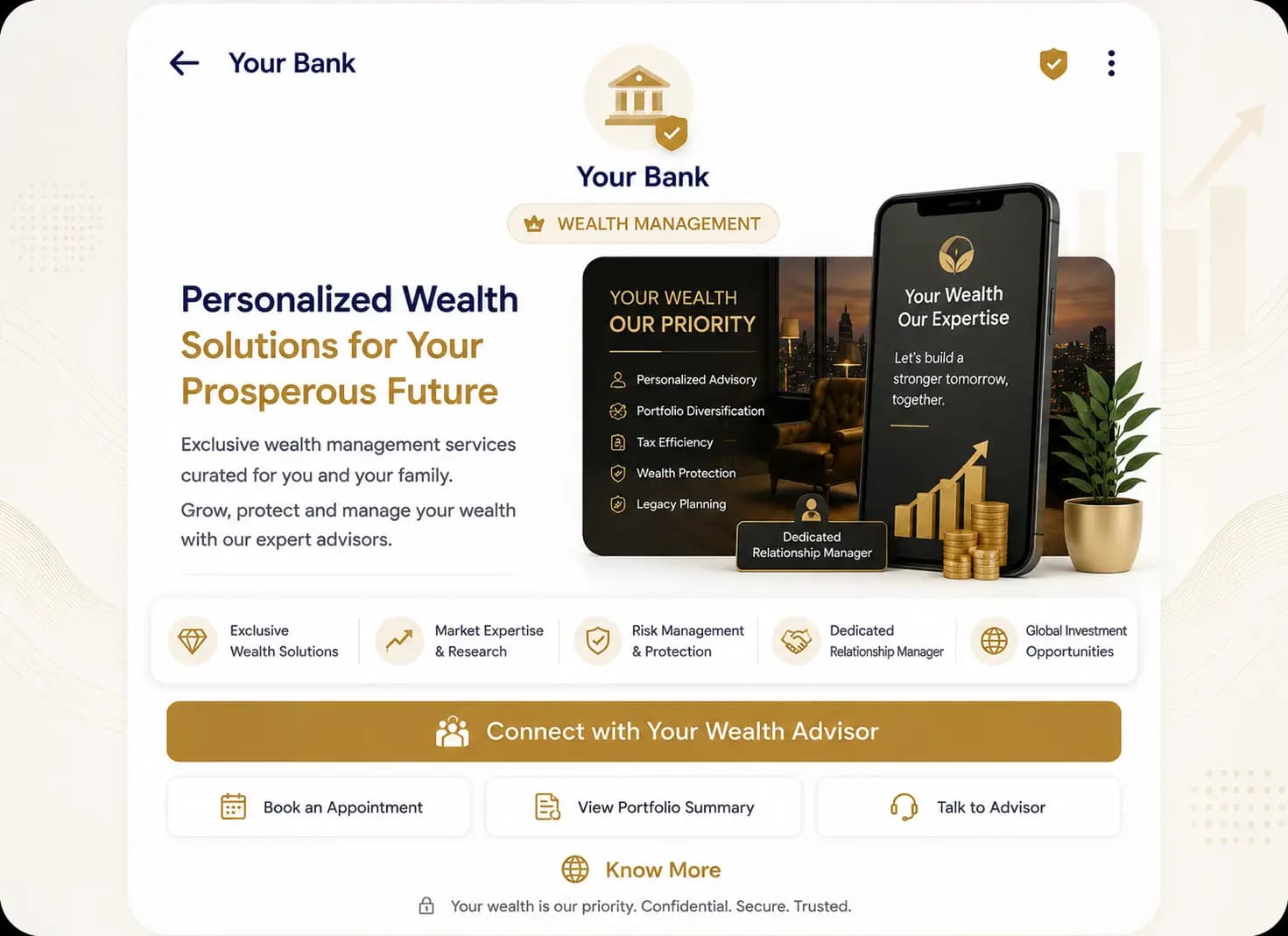

Trigger: High Net Worth Individual (HNI) and Ultra HNI segment. Quarterly portfolio review reminder, exclusive product pre-launch.

RCS format: Single premium rich card (not carousel — exclusivity signal). Personalised: client name, portfolio value, performance summary, exclusive offer. Buttons: 'Schedule Portfolio Review', 'Call My RM Now'.

Result: RM meeting scheduling rate: +3.8x vs email. Revenue per HNI RCS touchpoint: ₹18,000 (attributed product purchase). HNI engagement score: highest channel for relationship maintenance.

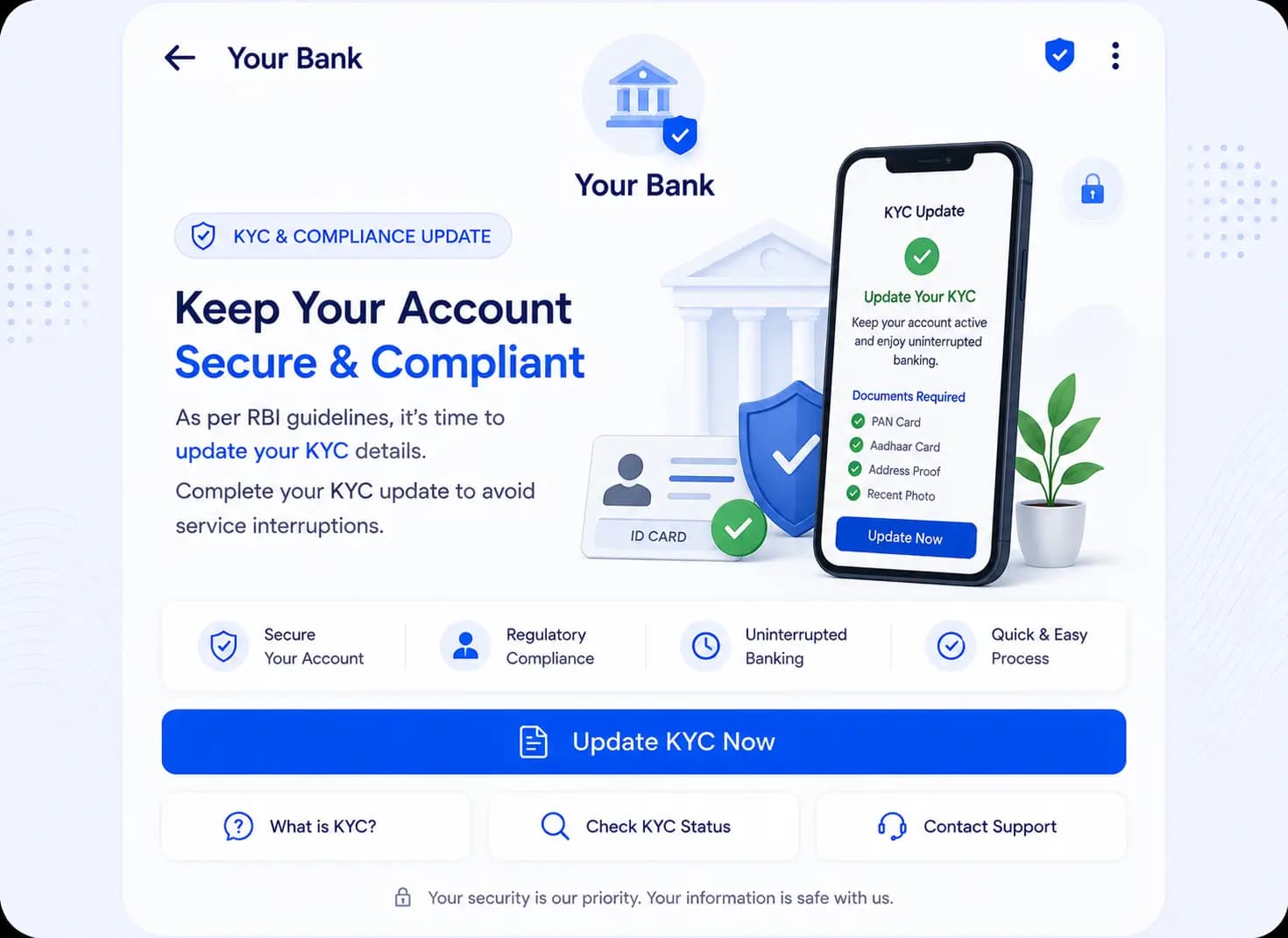

Trigger: Annual KYC renewal reminder, document expiry alert, or regulatory compliance communication from bank.

RCS format: Rich card: bank logo + verified, KYC status, what needs updating, deadline, 2 buttons: 'Update KYC Online' (links to video KYC or e-KYC portal), 'Visit Branch'. SMS fallback ensures 100% compliance reach.

Result: KYC completion rate via RCS: 61% vs SMS 22%. 'Update Online' button reduces branch load by 47%. Non-compliant account freeze rate: reduced 38% in pilot branches.

Compliance is non-negotiable for Indian financial services communication. Here is the complete regulatory picture for RCS messaging in the BFSI sector.

| Regulation | What it covers | Applies to RCS? | GCM handles |

|---|---|---|---|

| TRAI DLT | Entity registration, Sender ID, SMS template pre-approval | No — RCS is not regulated as commercial SMS | RCS bypasses DLT entirely. SMS fallback uses DLT-compliant templates. |

| TRAI DND | Do Not Disturb registry — limits promotional SMS reach and timing | No — RCS not classified as commercial SMS | RCS reaches DND-registered customers. No time restriction. |

| RBI Guidelines on Digital Comms | Fraud disclosure, customer consent, data security for banking comms | Partial — consent and data security apply | GCM provides consent management, encrypted data, India-hosted infrastructure. |

| Google RBM Policy | Brand verification, prohibited content (gambling, alcohol, adult) | Yes — all senders must comply | GCM reviews all banking templates for RBM policy compliance before submission. |

| IT Act / DPDP 2023 | Personal data handling, consent, right to erasure | Yes — applies to all digital comms | GCM platform includes opt-out management and data deletion on request. |

| PCI DSS | Payment card data security for card-related messaging | Partial — no card data in RCS messages | GCM never transmits card numbers. Payment links go to bank's PCI-compliant portal. |

| SEBI (for investment messaging) | Disclosure requirements for mutual fund/stock messaging | Yes — for investment product messaging | GCM provides disclosure text insertion in templates for SEBI-regulated products. |

Key compliance insight: RCS offers Indian banks a significant compliance advantage over promotional SMS: no DLT registration required for RCS message content, no DND restrictions, and no 9 AM–9 PM sending window. Banks can run pre-approved loan campaigns at 7 AM to customers on the DND registry — legally and with full brand verification.

SMS phishing (smishing) targeting Indian bank customers is a ₹1,000+ crore annual problem. RCS eliminates this attack vector entirely through Google's brand verification process.

Result: Banks running RCS report 43% reductions in phishing-related inbound support calls within 6 months of RCS launch — as customers learn to distinguish verified RCS messages from fraudulent SMS.

| Lifecycle Stage | RCS Message Type | Key Content | CTA Button | Business Goal |

|---|---|---|---|---|

| Acquisition | Pre-approved offer card | Product, rate, USPs, eligibility | Apply Now | New product activation |

| Onboarding | Welcome + setup guide | Account details, digital banking steps | Complete Setup | Activate digital banking |

| Early engagement | Product recommendation | Cards/loans/investments suited to profile | Explore Products | Cross-sell in first 90 days |

| Active usage | Transaction alerts | Verified transaction details, balance | Confirm / Block | Real-time fraud prevention |

| Cross-sell | Investment/insurance offer | Product benefits, returns, premium | Invest Now / Insure | Revenue per customer increase |

| EMI servicing | Payment reminder | Amount due, due date, account details | Pay Now | Reduce delinquency |

| Renewal | Insurance/FD renewal | Policy/FD details, renewal benefit | Renew Now | Prevent lapse |

| Problem resolution | Fraud alert | Transaction details, location, time | Confirm / Block | Reduce fraud loss |

| Dormancy | Reactivation offer | Balance, incentive, deadline | Reactivate | Reduce dormancy rate |

| Relationship | HNI portfolio review | Performance, exclusive access, RM contact | Schedule Review | Deepen HNI relationship |

| Campaign Type | SMS Performance | RCS Performance | Uplift |

|---|---|---|---|

| Credit card application rate | 0.9–1.3% | 5.5–7.2% | 5–6x higher |

| Personal loan conversion rate | 1.7–2.1% | 7.8–9.4% | 4–5x higher |

| EMI on-time payment rate | 61% | 82% | +21 percentage points |

| Fraud alert response rate | 11% | 68% | 6x higher |

| FD/investment booking rate | 0.7% | 3.8–4.5% | 5x higher |

| Insurance renewal rate | 54% | 81% | +27 percentage points |

| KYC completion rate | 20–24% | 58–64% | 3x higher |

| Account reactivation rate | 2.1% | 12–16% | 6–7x higher |

| Phishing support calls (6mo) | Baseline | -43% | Significant reduction |

| Read rate (overall banking RCS) | ~35% est. | 89% tracked | 2.5x higher |

Data note: Performance figures are based on aggregated data from Indian BFSI RCS deployments. Actual performance varies by product type, customer segment, message quality, and send timing.

Priority use cases: Credit card acquisition campaigns, pre-approved loan offers targeted by credit score band, investment product cross-sell, HNI relationship management.

Key priority: Build RCS into CRM triggered-communication stack — not treat as separate blast channel.

Priority use cases: KYC compliance communication, dormant account reactivation, Jan Dhan and PM scheme-linked communication, loan EMI reminders for rural and semi-urban borrowers.

Key priority: Robust SMS fallback for 2G/3G customers. Focus on compliance and customer outreach.

Priority use cases: Pre-approved loan offers, EMI reminders, collections communication (verified sender adds seriousness), insurance cross-sell bundled with loan products.

Key priority: High acquisition cost environment — clear ROI advantage of RCS-driven loan conversion over SMS.

Priority use cases: Multi-touch renewal reminder series (30/15/7/1 day), lapse reactivation campaigns, annual premium payment reminders, health policy renewal with sum insured enhancement.

Key priority: 3-card carousel (policy summary / lapse risk / renew now) is the highest-converting format.

Priority use cases: Quarterly portfolio performance cards, exclusive product pre-launch invitations, SIP reminder and top-up nudges, RM-initiated relationship touchpoints.

Key priority: Verified sender identity is particularly important — HNI clients have high fraud sensitivity.

RBI-aligned compliance framework

India-hosted infrastructure, templates reviewed for RBI digital communication guidelines, SEBI-mandated disclosure text insertion for investment products.

Direct Jio and Airtel carrier integration

Fastest delivery, most accurate capability detection, lowest SMS fallback rates — critical for fraud alerts where latency matters in seconds.

Real-time API for transaction-triggered messaging

Sub-second trigger-to-delivery latency. Supports concurrent high-volume API calls with SLAs for financial services.

Dedicated BFSI account management

Account managers with specific financial services experience. Understand regulatory environment, CRM systems, and compliance review processes.

Proven performance with Indian financial brands

Deployed RCS campaigns for banking, NBFC, and insurance clients across India. Anonymised performance benchmarks from comparable institutions.

RCS Business Messaging eliminates the spoofed Sender ID attack vector that drives most banking SMS fraud in India. Every RCS message is sent through Google's verified RBM platform with the bank's verified name, logo, and a verification indicator — which cannot be replicated by fraudsters. Banks report 43% reductions in phishing-related support calls within 6 months of RCS launch as customers learn to distinguish verified RCS messages from fraudulent SMS.

No. RCS Business Messaging is not classified as commercial SMS under TRAI's Telecom Commercial Communications Customer Preference Regulations. Banks do not need DLT entity registration, Sender ID registration, or template pre-approval with TRAI for RCS messages. Banks must complete Google's brand verification process instead — which Get Click Media handles as part of onboarding. If banks also send SMS (for fallback or other use cases), DLT registration remains mandatory for those SMS messages.

Yes. RCS is not subject to TRAI's DND (Do Not Disturb) restrictions that limit promotional SMS. Banks can send marketing RCS messages to DND-registered customers — including credit card offers, loan campaigns, and investment product promotions — as long as standard marketing consent is in place. This is a significant regulatory advantage over promotional SMS, which cannot legally reach DND-registered numbers.

Yes. Real-time fraud alerts are one of RCS's highest-value banking applications. Get Click Media's API supports sub-second trigger-to-delivery for transaction-triggered messages. A fraud alert RCS message with quick-reply chips ('Yes, this was me' / 'No, block this transaction') achieves 68% customer response rates vs 11% for equivalent SMS alerts — dramatically improving fraud detection speed and reducing false positive freezes.

RCS messaging, when properly implemented, aligns with RBI's digital communication guidelines for financial services. Key compliance requirements that apply to RCS include: customer consent for marketing communication, opt-out management, no transmission of sensitive payment card data in messages, and data security for personal financial information. Get Click Media's platform addresses all of these requirements, with India-hosted infrastructure and DPDP 2023-aligned data handling.

For banking customers in rural and semi-urban areas — who may be on BSNL, on 2G connectivity, or using feature phones — RCS automatically falls back to SMS. Get Click Media's platform detects device capability in real time and routes to SMS when RCS is unavailable. Banks define both the RCS version and the SMS fallback version in a single campaign setup. The SMS fallback is billed at standard SMS rates. This ensures that compliance-critical communication (KYC reminders, EMI alerts) reaches 100% of customers regardless of device or network.

ROI varies by use case. Credit card acquisition campaigns typically show 4x to 6x higher application rates vs SMS at comparable cost per message — translating to 70–80% lower cost per activated card. Personal loan campaigns show similar conversion improvement. EMI reminder campaigns improve on-time payment rates by 20+ percentage points, directly reducing provisioning costs. For a mid-size Indian private bank sending 50 lakh messages per month, switching from SMS to RCS typically delivers ₹2–5 crore per month in improved conversion value.

Yes. Any Indian financial services company — bank, NBFC, insurance company, stockbroker, wealth manager, or fintech — can use RCS Business Messaging through Get Click Media. The Google brand verification process requires a legitimate registered business entity, which all licensed BFSI companies have. NBFCs often achieve higher RCS ROI than banks because their cost of customer acquisition is higher and the uplift from verified, visual messaging is proportionally more valuable.

Get Click Media handles Google brand verification, compliance review, and campaign setup. Most BFSI clients are live within 7–10 business days.